There is a quiet trap in the way rewards cards get sold, and a lot of careful people walk straight into it. The pitch is simple and appealing. Spend like you normally would, earn points or cash back on every purchase, and let the card pay you for the privilege. That math works beautifully right up until you carry a balance from one month to the next. The moment you do, the rewards stop being free money and start being a small discount on a much larger bill. Understanding why is the difference between a card that works for you and one that quietly drains you while it pretends to be generous.

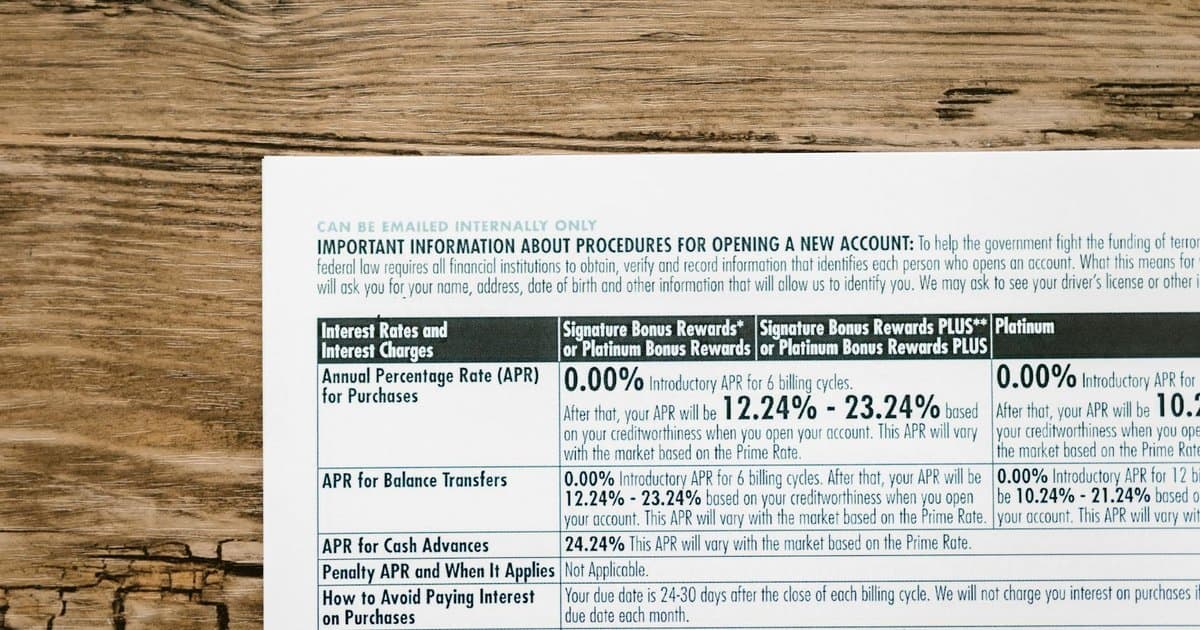

Start with the two numbers that matter most. A strong rewards card might pay you two percent back on your spending, and some categories pay more. That same card, on average right now, charges well over twenty percent in interest on any balance you carry. Those numbers are not in the same league. You are earning two cents on the dollar while paying more than twenty cents on the dollar for the part you did not pay off. The reward rate and the interest rate are pointed in opposite directions, and the interest rate is roughly ten times larger, so any month you carry a balance, the card is taking far more than it gives.

Run a normal household through it and the trap gets concrete. Say you spend two thousand dollars a month on the card and earn two percent, which is forty dollars in rewards. Now say you carry a three thousand dollar balance month after month at twenty four percent interest. That balance costs you about sixty dollars in interest every single month. So you collect forty in rewards and pay sixty in interest, and you are twenty dollars underwater before you have bought anything new. The longer that pattern runs, the worse it gets, because interest compounds while rewards do not.

This is why comparing cards by their rewards rate is the wrong first question for anyone carrying a balance. People agonize over whether to get the card that pays three percent on groceries or the one that pays four percent on travel, when the rewards gap between them is rounding error next to what interest is costing them. If you are paying interest, the best financial move available is not a better rewards card. It is paying the balance down to zero, because eliminating a twenty four percent cost is the same as earning a guaranteed twenty four percent return, and nothing in the rewards world comes close to that.

The stakes climb fast when the balance becomes a habit instead of an emergency. A one time slip, paid off quickly, costs you a few dollars and a lesson. A balance you carry indefinitely turns the card into a slow leak that follows you for years. People in this spot often keep spending to chase points, telling themselves the rewards soften the blow, when in reality the spending is feeding the very balance generating the interest. The card has trained them to do the one thing that benefits the card. Breaking that loop is not about willpower around purchases. It is about seeing clearly that the rewards were never the prize. The balance was always the cost.

So the rule is blunt and worth saying plainly. Rewards cards are only a good deal if you pay the statement balance in full every month, every time, without exception. Used that way, the points and cash back are genuinely free, a real benefit for spending you were doing anyway. Used any other way, the card is one of the most expensive forms of borrowing a normal person has easy access to, and the rewards are a thin layer of sugar on top of a steep price. The card does not care which version of you shows up. It pays out the same either way and collects far more from the version that carries a balance.

If you are carrying one right now, the path forward is not complicated, just uncomfortable for a stretch. Stop charging new spending to that card and switch to a debit card or cash until the balance is gone, so you are not adding to the pile while you try to shrink it. Throw every spare dollar at the highest interest balance first, since that is the one costing you the most. Once you hit zero, you can go back to using the rewards card freely, paying it in full each month, finally on the side of the deal where the points are actually worth chasing. Until then, the most rewarding thing your card can do is sit unused while you dig out.